← Back to Insights

Aclymate Team

November 20, 2025

California has taken a major step toward climate transparency with Senate Bill 261 (SB 261). This law requires large companies to share how climate change may affect their financial stability.

If your business operates in California and earns more than $500 million a year, this law directly applies to you. Understanding it early helps you stay compliant, protect your brand, and build trust with investors and customers. Even if the law doesn’t apply to you, but it does apply to your suppliers or customers, it will likely affect you.

This article breaks down the scope, importance, and requirements of SB 261. We'll also discuss how your company can prepare before it takes full effect in 2026.

SB 261, also known as the Climate-Related Financial Risk Act, requires large business entities operating in California to report how climate-related risks may affect their financial performance.

The act adds Section 38533 to the Health and Safety Code, which relates to greenhouse gases (GHG).

Under the California Air Resources Board (variably known as ARB, CA ARB, or CARB)'s authority, SB 261 mandates that “covered entities” should prepare and publish a climate-related financial risk report on or before January 1, 2026, and biennially thereafter.

The report must address physical and transition threats, how these risks might harm immediate or long-term financial outcomes, and what measures the company has adopted to reduce or adapt to those risks.

SB 261 applies to U.S. companies doing business in California that have global annual revenues greater than $500 million based on the prior fiscal year.

It covers both public and private entities that meet the revenue threshold, even if they’re headquartered outside California but operate within the state.

According to the FAQs shared by CARB, "doing business in California" means the following:

Meanwhile, the bill text states that companies subject to regulation by the Department of Insurance in California or insurance businesses in any other state are exempted from SB 261.

If you're unsure whether you need to comply with SB 261 or not, the CARB shared a preliminary list of covered entities.

You can refer to that list or voluntarily submit your company name through this CARB survey if you believe you're subject to SB 261. You can also complete the same survey if you qualify for an exemption.

Here are the key dates you should know if you're curious about how SB 261 was established and when you need to submit the first report.

SB 261 is important because it turns climate transparency into a legal duty for major businesses.

The act requires mandatory disclosures of climate-related financial risks, subjecting companies to treat environmental impact as part of financial reporting. Thousands of businesses now disclose their climate-related financial risks.

It aims to enhance transparency and accountability around how climate change could affect daily operations, supply chains, and financial outlook.

For investors, regulators, and the general public, SB 261 helps them understand financial exposures tied to various climate scenarios.

Failure to comply can trigger civil penalties. This climate inaction can cost your business up to $50,000 per year.

On the positive side, sharing public disclosures in compliance with SB 261 can boost your brand credibility. You can also open the door to new partnerships, strengthen relationships with other stakeholders, and meet consumer demand.

Under SB 261, companies operating in California should prepare a climate-related financial risk report every two years starting on January 1, 2026.

The report must provide clear, credible climate information about how environmental factors affect financial performance.

The California Air Resources Board released draft guidance through a checklist that outlines what to include.

Each disclosure should describe the company’s governance structure, physical impact, transition risks, and the measures adopted to reduce those risks.

Make sure to identify metrics and targets used to track progress and disclose how you manage climate-related risks.

Don't forget to publish the report on your website and submit the public link to CARB's docket.

You should also pay an annual fee to CARB. The estimated flat annual fee is $1,403 for SB 261 entities. The price will adjust every year for inflation.

SB 261 is not the only climate disclosure act that California passed. The state also enacted another major climate reporting law called the Climate Corporate Data Accountability Act (SB 253).

Both SB 261 and SB 253 work together, but they cover various aspects of climate accountability. Below is a quick comparison to help you understand how they differ:

| SB 261 | SB 253 | |

|---|---|---|

| Applicability | Companies doing business in California with over $500 million in global annual revenue. | Corporations operating in California with over $1 billion in global annual revenue. |

| Reporting period and deadline | The first climate-related financial risk report is due January 1, 2026, and updated every two years. | The first GHG emissions disclosure is due in 2026 (Scope 1 & 2) and 2027 (Scope 3 indirect emissions). |

| Oversight Agency | California Air Resources Board | California Air Resources Board |

| Assurance Requirements | None | SB 253 requires third-party assurance |

| Penalties | Civil penalties up to $50,000 per reporting year for failing to publish a climate-related financial risk report. | Administrative penalties up to $500,000 per year for failing to report greenhouse gas emissions data. |

Here are some tips to help you comply with SB 261, based on the draft checklist released by CARB.

Decide which reporting structure you will follow. Under SB 261, you can choose from the following sustainability standards and frameworks:

Add a brief statement that explains which reporting framework you applied. Then, list the recommendations and disclosures that have been compiled and which have not, based on your chosen framework.

In case you haven't included recommendations or disclosures, explain the reasons why. You should also discuss any plans for future disclosures.

The next step involves outlining your company’s governance structure for addressing climate-related financial risks. This is considered the minimum CARB requirement.

Disclose who in your organization oversees climate issues (board, executive, or risk committee) and how climate-risk management ties into your organization’s strategy.

Identify the actual and potential impacts of climate-related risks on your current operations, strategy, and financial planning. Consider the short-, medium-, and long-term risks.

You can use climate scenarios to support disclosures in compliance with SB 261.

However, CARB encourages the inclusion of a qualitative scenario-based assessment or any advanced method where suitable.

Your report should do more than describe climate-related financial risks. You must also disclose how you manage these risks.

Explain detailed processes for identifying, assessing, and mitigating climate-related financial risks. Then, show how these processes integrate into your overall risk management strategy.

Narrative sections of your report describe risk and strategy. However, metrics and targets turn that information into useful, consistent, and forward-looking data for stakeholders.

That's why it's important to disclose metrics used to assess and manage relevant climate-related risks. You should also document the opportunities adopted to reduce and adapt to these risks.

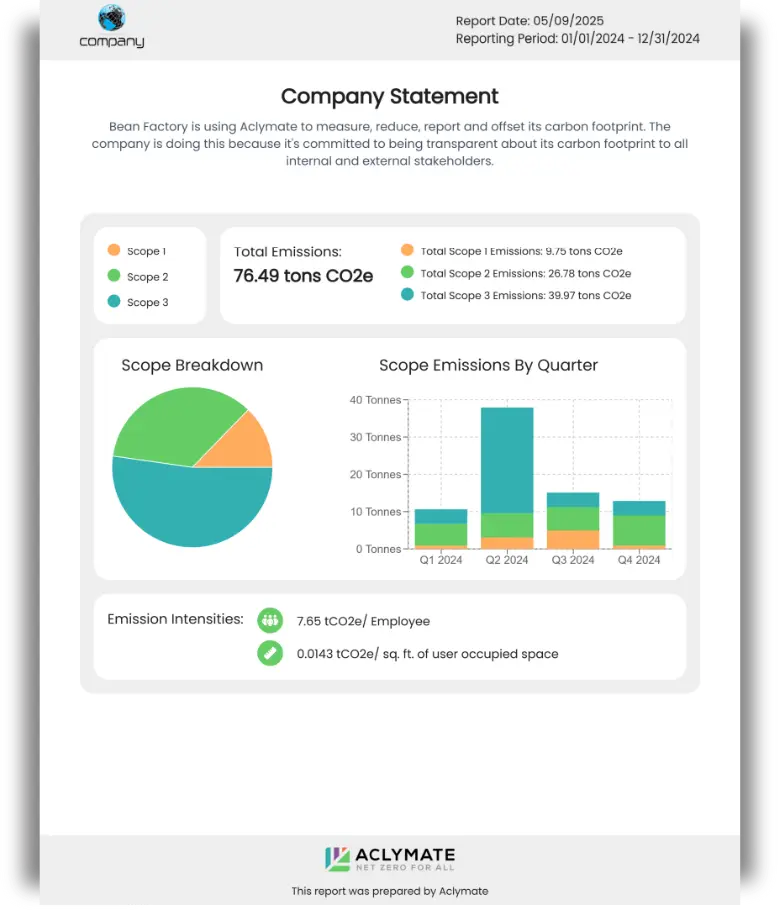

Although full emissions disclosure (Scope 1, 2, and 3) is not a requirement for the initial report, it is considered a best-practice to include it.

After preparing and finalizing your report, publish it on your company’s website. Then, submit the URL to CARB’s public docket within the defined period.

Make sure the link remains accessible, so stakeholders and the public can easily access it. This marks your formal compliance under SB 261.

Are you a California business preparing to meet your SB 261 obligations? Aclymate is here to help you report with confidence.

Its Turn Key solution gives you a designated carbon bookkeeper who handles every detail for you, from data entry to public disclosure. Climate consultants will become your sustainability team without the consultant-level price.

Want to do it yourself? Aclymate's user-friendly sustainability management software makes it easy. It simplifies climate reporting with automated data collection, AI-powered categorization, and audit-ready outputs. Save time and ensure compliance with the evolving rules of SB 261.

Book a demo to learn how Aclymate's experts and intuitive solutions can help you.

SB 261 is required for California-operating companies whose annual gross revenue exceeds $500 million. This threshold covers both private and public businesses, including those headquartered outside the state. However, certain entities, like insurance companies, are exempted.

SB 261 requires companies to publish a climate-related financial risk report that explains how environmental factors could impact their finances. The report must also describe risk management efforts, including scenario analysis and the measures taken to adapt or reduce risks. The goal is to provide stakeholders with transparent, decision-ready climate information.

Companies that fail to comply with SB 261 may face civil penalties imposed by the California Air Resources Board. Fines can reach up to $50,000 per reporting year.

To comply, companies need to identify climate-related financial risks, prepare a compliant report under a framework such as TCFD, and publish it publicly by January 1, 2026. The report should cover governance, strategy, risk management, and metrics. Businesses must then post the report’s link on the CARB public docket.

Your customers will need to identify risks to their supply chain, which includes your business. Your customers will, at a minimum, be requesting the physical location of your facilities, but also may ask for your corporate carbon accounting, any climate-related risk analyses you have completed, and potentially even the product carbon footprint of what they purchase from your company.

Get Aclymate's practical sustainability content delivered weekly.

AI can make Scope 3 reporting faster by organizing supplier data, identifying gaps, and drafting communications. But it can't replace GHG Protocol methodology, verified supplier data, or expert judgment. The strongest Scope 3 programs use AI to support the process, not replace it.

Read Article

AI can help small and mid-sized businesses kickstart sustainability by organizing data, drafting policies, and generating ideas. But credible reporting still depends on accurate emissions calculations, recognized methodologies, and purpose built carbon accounting software.

Read Article

AI can help write sustainability content, but it can't prove your claims. Learn why credible sustainability messaging depends on real data, auditability, and third party verification, not AI generated copy alone.

Read Article

Talk with a Sustainability Expert, see a demo, or start free to put the Aclymate platform and experts to work for your team.